How to Create a Budget in 7 Simple Steps

These in-depth tips will help you create a budget and manage your money more effectively.

Key Takeaways

- Print off the last 90 days of your bank statements to find your average monthly spending in various categories.

- Choose the budgeting plan that fits your needs: 50/30/20 or zero-based budgeting.

- Stick to budgeting for at least 90 days. The first few months may be rough, but you should start to settle into a flow by Month 3.

How are we ever going to get caught up with the bills?

Has this thought ever popped into your mind before? If this is you, the truth is you're not alone. In fact, you are part of the almost 80% of the U.S. workforce who report that they currently live paycheck to paycheck. 1

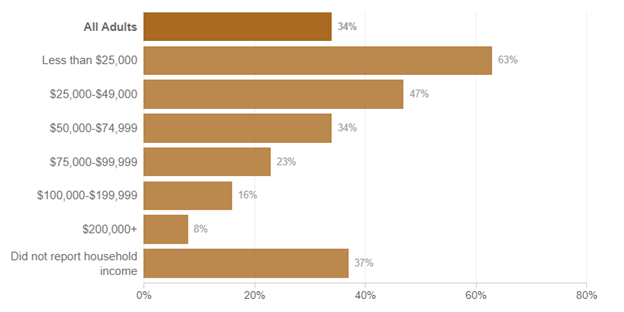

Of course, the first thought that comes to mind is that you just need to make more money, right? Well, not so fast. A recent report breaks down the percentage of adults stating they are struggling making necessary expenses such as food, rent or mortgage, car payments, medical expenses or student loans as compared to their annual income.

Source: NPR: Paycheck-To-Paycheck Nation: Why Even Americans With Higher Income Struggle With Bills 2

As you can see above, even those making $100,000 or more per year are living paycheck to paycheck and struggling to make the payments for the basic needs in their lives.

So, how do I stop living paycheck to paycheck with my current income?

The good news is the answer is simpler than you may realize. The absolute best way to stop living paycheck to paycheck is to create a plan for the money coming into and out of your life.

As Zig Ziglar famously said, “If you aim at nothing, you will hit it every time.”

Why do you need a budget?

A budget serves as a financial roadmap, providing you with a clear picture of your income, expenses, and savings goals. It empowers you to take control of your finances, reduce financial stress, and work towards achieving your goals. Whether you want to pay off debt, build your emergency savings, or save for a new car , a budget can help you get there.

The Benefits of Budgeting

Still need convincing? Here are 5 reasons to create a budget and stick with it.

- Budgeting can help you handle financial emergencies: If your budget includes an emergency fund, you're less likely to rack up debt when a stressful financial situation hits. You won't feel as side-swept losing that money for an emergency expense when it's already budgeted for.

- Budgeting can help you prepare for retirement: A budget will help you figure out how much you can afford to contribute to your retirement fund and keep you consistent with making those contributions.

- Budgeting makes you aware of your spending habits: Knowing where your money is going each month makes you think twice about every purchase. By reviewing your expenses every month, you'll see where you can make some changes in your spending habits.

- Budgeting empowers you to make financial decisions: When you maintain a budget, you're highly aware of what you can afford. You're aware of your financial goals and the work it's taking to get there. This means you're in control of your money, rather than the other way around.

- Budgeting helps reduce stress: Let's face it – money can be a triggering topic that comes with a lot of baggage. When you feel out of control with your spending, it affects your whole life. Conquering your finances, however, can reduce your stress, enhance your overall wellbeing and even improve your relationships.

Related content:

One Couple, One Budget: How to Combine Finances in a Relationship

How to Create a Budget

- Analyze your past 90 days of spending.

- Create spending and saving categories.

- Transfer your spending into a budget template.

- Choose a budgeting method.

- Stick to your plan for 90 days.

- Review and adjust as needed.

- Make budgeting a lifestyle.

Before we create any kind of change in life, we need to draw a line in the sand; the starting line. The first step is that line.

Step 1: Print off 90 days' worth of bank statements

Before you can tell your money what to do, you need to find out what the money has been doing. To start off, print off the last three months of all bank statements. Anywhere money comes into your accounts and then leaves your account needs to be printed off. This includes checking account statements and all credit card statements.

Step 2: Create spending and saving categories.

Next, go through all of your expenses from your statements and look for common themes of spending.

You should notice the obvious ones, such as rent or mortgage, car payment, insurance and your cell phone bill. But then you'll want to start grouping expenses you see into other categories you have in your life.

Do you have a lot of dining out expenses? Are there expenses from grocery shopping, department store shopping, or other themes you notice?

Download our Free Budget Worksheet to get started.

Some common categories include:

- Groceries

- Dining Out

- Fuel

- House Expenses

- Car Expenses

- Health and Beauty

- Kids

Pro Tip: Limit your categories to no more than 20. In fact, the fewer the better.

Average of the 90 days

After you have added up all your expenses for each category over the last 90 days (three months), it's time to get the monthly average.

Example: If you added up three months' worth of grocery expenses and the total is $1,500, then your monthly expense for groceries is $500.

Repeat this for all categories you created.

Keep in mind you are just creating a baseline based on the past 90 days of expenses. This is not a perfect science (yet), but for now it gives you a great starting point.

Step 3: Transfer your spending into a budget template.

Now that you know where the money has been going, it's time to transfer that into your own budget.

You can grab our free budget form here .

Start with your take-home pay.

The very first number you are going to enter into your budget is your take-home pay. This is NOT how much you earn each month, but rather how much actually hits your checking account each month after taxes, benefits and retirement contributions are taken out.

It doesn't matter whether you get paid weekly, bi-weekly or monthly. Simply add up how much you take home each month and enter that into the “Income” section of your budget.

Enter in the categories.

Next, start entering in the categories you created from step 2, and the monthly average for each category based on the 90-day totals you calculated.

You will notice some of your expenses are “fixed”, meaning they are the same amount each month. This will likely be your mortgage/rent, car payment, cell phone bill, subscriptions or anything else that remains the same.

The rest are your “flexible” expenses, meaning they fluctuate each month. Your power bill may be higher in the summer, while your fuel costs will fluctuate with the cost of gas prices.

Related content:

Step 4: Choose a budgeting method.

Okay, now comes the official “budgeting” work.

- Zero-Based Budget: With a zero-based budget, you'll assign every dollar a specific purpose, ensuring that your income minus expenses equals zero. This method promotes conscious spending and eliminates excess.

- 50/30/20 Budget: Using the 50/30/20 budgeting strategy, you'll allocate 50% of your income to needs, 30% to wants, and 20% to savings. This approach gives you a sense of structure for your spending and saving priorities.

Step 5: Stick to your plan for 90 days.

Once you have created your zero-based budget, it's now officially time for you to follow the plan you created for yourself.

Think about this: for most Americans who are paycheck to paycheck, money is always in control of their lives. They are constantly thinking or stressing about how to make the next bill payment or trying to time the due date with the next paycheck.

This officially stops right now.

At this step you have looked back 90 days and given yourself a great estimate of how much you spend in different areas of your life. Then you ironed out the wrinkles to make sure your income will cover all the expenses you plan to make.

Now, each time you make a payment, or an expense occurs, simply enter it into the budget you just created. When you make the rent payment on the first of the month, go ahead and enter that amount in. Or when you leave the checkout at the grocery store, hold onto the receipt and enter that amount into your budget.

Pro Tip: Always ask for a receipt. At the end of the day, spend the two to three minutes entering those totals into your budget. Also, round up your expenses for easy math and to create a little buffer in your checking account. Instead of $33.82 on gas, make it an even $34.

Step 6: Review and adjust as needed.

One of the most important parts of creating a budget is realizing you will never be perfect. So many people start a budget, feel like a failure, and unfortunately quit.

Don't let this happen to you.

Yes, you're going to be really close on some of the expense categories you created, and you will also be way off on others. This is completely normal, and it happens to everyone.

You will forget about certain categories halfway through the month, you may miss a few expenses, and you will likely overspend that first month.

If this happens to you, remember this is completely normal. If it were easy right away, the entire country would live on a budget, right?

Step 7: Make budgeting a lifestyle.

Month one is going to feel like a disaster for some. You'll probably have 37 emergency budget meetings and may even get a little worked up over it.

The second month, you'll make adjustments based on the mistakes from the previous month. By the third month, you will be a budgeting all-star.

Any time we make a change in our lives, it's not going to start off perfect or the way we expect. This is why you must rinse and repeat the budgeting process until you start to feel comfortable with it.

By sticking with it, you'll transform budgeting from a temporary task into a lifelong habit. Embrace the financial discipline and mindfulness that budgeting brings to secure a stable financial future.

The Result of Your Budget

The one thing that will shock you is how much you have been spending in certain categories. You may also surprise yourself and find money you didn't even know you had inside your budget.

When my wife and I first started our monthly budget process, it was ugly. We were pulling in two different directions and that first month it felt like the budget was an absolute disaster.

Then, the second month, we made a few tweaks and by month three we were smooth sailing.

In fact, today it takes us about five minutes per month to create our budget. We usually do this on the last day of the month to forecast and prepare for the upcoming month.

Saving more money

We noticed those first few months we were saving around $500 per month by creating a plan for our money and following it. This means we were able to give ourselves a $6,000 per year raise without having to work extra hours or pick up a second job.

This was simply by creating a plan, following the plan and improving the plan.

Because we now pay attention to the dollars and cents in our life, we no longer pay interest—we earn interest.

Creating a Budget FAQs

Cash stuffing refers to setting aside physical cash in envelopes for specific spending categories, helping you control discretionary expenses and avoid overspending.

Beginners can start by tracking their spending, creating basic spending categories, and gradually introducing budgeting methods like the zero-based budget or the 50/30/20 budget.

To create a monthly budget, list your expected income, allocate funds to various categories based on your spending and savings goals, and adjust as needed throughout the month to stay on track. Use a budgeting template to help you see the full picture.

It's your turn to get the money right. Start by creating your own budget today.

APR = Annual Percentage Rate